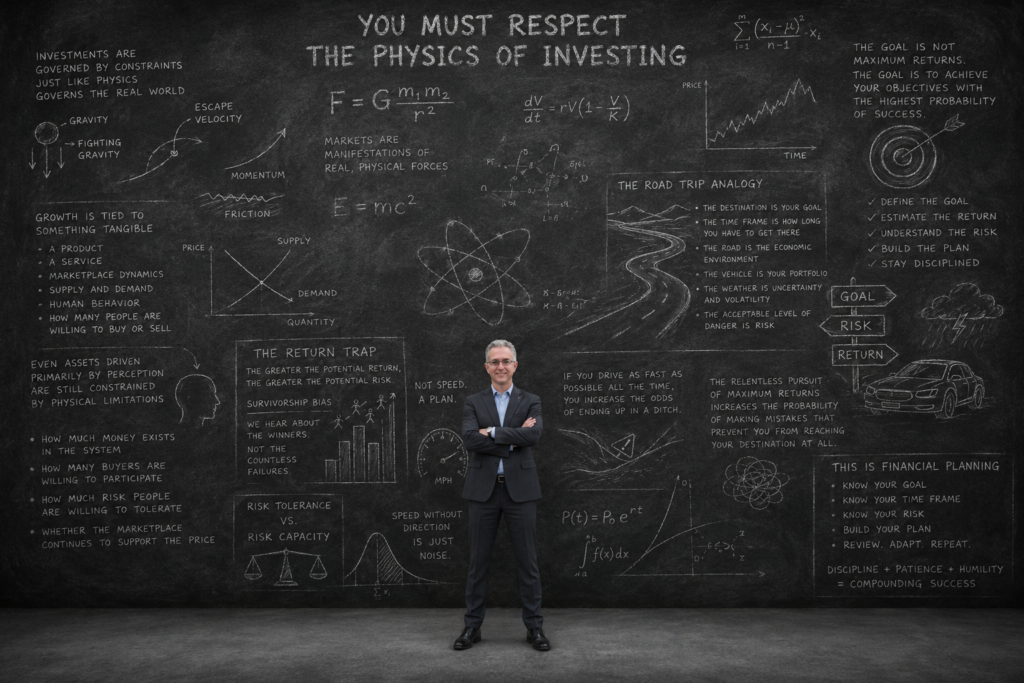

You Must Respect the Physics of Investing

The Physics of Investing

Investments are governed by constraints, just like physics governs the real world.

Some investments spend years fighting gravity.

Some achieve escape velocity.

Some develop tremendous momentum.

Others encounter friction that prevents them from ever reaching their potential.

One of the most dangerous ideas in investing is the belief that you can separate returns from the Physical reality that creates them. You cannot.

You must respect the physics of investing.

Investing can sometimes feel abstract or ethereal, but capital markets are manifestations of very real, very physical forces. The stock market may seem detached from reality at times, but it is not detached from the laws that govern reality.

The growth of an asset is tied to something tangible:

a product,

a service,

marketplace dynamics,

supply and demand,

human behavior,

or simply how many people are willing to buy or sell it.

Even assets driven primarily by perception are still constrained by physical limitations.

How much money exists in the system.

How many buyers are willing to participate.

How much risk people are willing to tolerate.

Whether the marketplace continues to support the price.

These are not abstract concepts.

These are constraints.

The physics of investing are real.

And yet many investors approach markets as though these constraints do not exist.

The Return Trap

Over the years, I have heard many versions of the same statement:

“I just want to make as much money as possible.”

There is nothing inherently wrong with wanting strong returns. Of course people want their money to grow. But making as much money as possible, by itself, is not a complete financial framework.

Why?

Because all investing involves risk.

And it is generally true that the greater the potential return, the greater the potential risk.

Survivorship bias distorts reality.

People hear stories about the stock that doubled overnight.

What they rarely hear about are the countless investments that failed, the businesses that disappeared, and the risks that never paid off.

This is simply a feature of selective memory and the information we are exposed to.

The more important question is not how much return you want.

The more important question is how much risk is appropriate.

The Road Trip Analogy

A useful way to think about this is through the analogy of travel.

Imagine you sit down with someone to plan a long road trip. They ask where you are trying to go, how long you have to get there, what roads you want to take, what conditions you may encounter, and how much risk you are comfortable accepting along the way.

And your response is:

“I don’t care about the road conditions, traffic, weather, braking distance, survivability, destination, or time frame. I just want to drive 120 miles per hour the entire time.”

You would immediately recognize that as irrational.

Because speed alone is not a plan.

You cannot intelligently determine how fast you should drive without first understanding:

the destination,

the time frame,

the road,

the vehicle,

the weather,

and the acceptable level of danger.

If you try to drive as fast as possible all the time, you increase the odds of ending up in a ditch, crossing the median, taking a turn too fast in the rain, hitting a divider, or missing your exit entirely.

This Is Financial Planning

This is literally financial planning.

The destination is your goal.

Retirement. Financial independence. Leaving money to your children. Supporting your lifestyle.

The time frame is how long you have to get there.

The road is the economic environment and market conditions you may encounter along the way.

The vehicle is your portfolio and the investments themselves.

The weather is uncertainty, volatility, recession, fear, euphoria, instability, and the reality that markets do not move in straight lines.

And the acceptable level of danger is risk.

This is why goals determine appropriate risk.

Because if you do not first define where you are trying to go, how could you possibly know what level of speed, danger, or risk is appropriate?

Another Lesson Hidden in the Analogy

And there is another lesson hidden in the analogy.

If you try to drive as fast as possible all the time, you increase the odds of ending up in a ditch, crossing the median, taking a turn too fast in the rain, hitting a divider, or missing your exit entirely.

The same thing happens in investing.

The relentless pursuit of maximum returns often increases the probability of making mistakes that prevent you from reaching your destination at all.

Those, too, are the physics of investing.

The Goal Is Not Maximum Returns

The goal is not to maximize returns.

The goal is to achieve your objectives with the highest probability of success.

Once you know where you are trying to go, you can estimate the return required to get there.

Once you know the required return, you can begin determining the amount of risk that may be necessary.

Investing is not about pursuing the highest possible return.

It is about pursuing the appropriate return.

This is the part many investors miss.

You should not simply guess how much risk to take and then manage your wealth without a plan.

Risk Tolerance vs. Risk Capacity

You can emotionally tolerate enormous amounts of risk while your financial life may have very little actual capacity for it.

Or you may personally dislike volatility while your financial plan demonstrates that you possess enormous flexibility and capacity to take risk safely.

This distinction between risk tolerance and risk capacity is one of the most important concepts in investing.

This is why intelligent investing requires humility.

Reality.

Calibration.

Awareness of consequences.

Why a Plan Matters

This is financial planning.

And if your finances are important to you, then it is wise to bring those principles into your investment framework.

You should not simply guess how much risk to take and then manage your wealth without a plan.

Because without a plan, there is no rational mechanism for determining how much risk is appropriate in the first place.

Advice without context is not advice.

It is guesswork.

The Question Every Investor Should Ask

You are allowed to pursue aggressive growth if that is what you choose.

You are allowed to drive fast.

But you must respect the physics.

Because the laws governing risk do not disappear simply because somebody wants higher returns.

And eventually, reality asserts itself.

So ask yourself:

Do I actually know where I am trying to go?

Is my current level of investment risk truly appropriate for getting me there?

Does my financial plan demonstrate my capacity to take risk?

Am I making decisions about risk based on a plan, or am I simply guessing?

Do I know the return I actually need, or am I chasing the return I hope for?

Am I taking risk in service of a goal, or taking risk for its own sake?

Because if you cannot answer those questions, you may not be investing according to a plan.

You may simply be driving fast and hoping you arrive.